Banks and You by Francis Turner

Q: What’s the difference between Hunter Biden, Konstantin Kisin and you?

A: Access to banks

Let me explain.

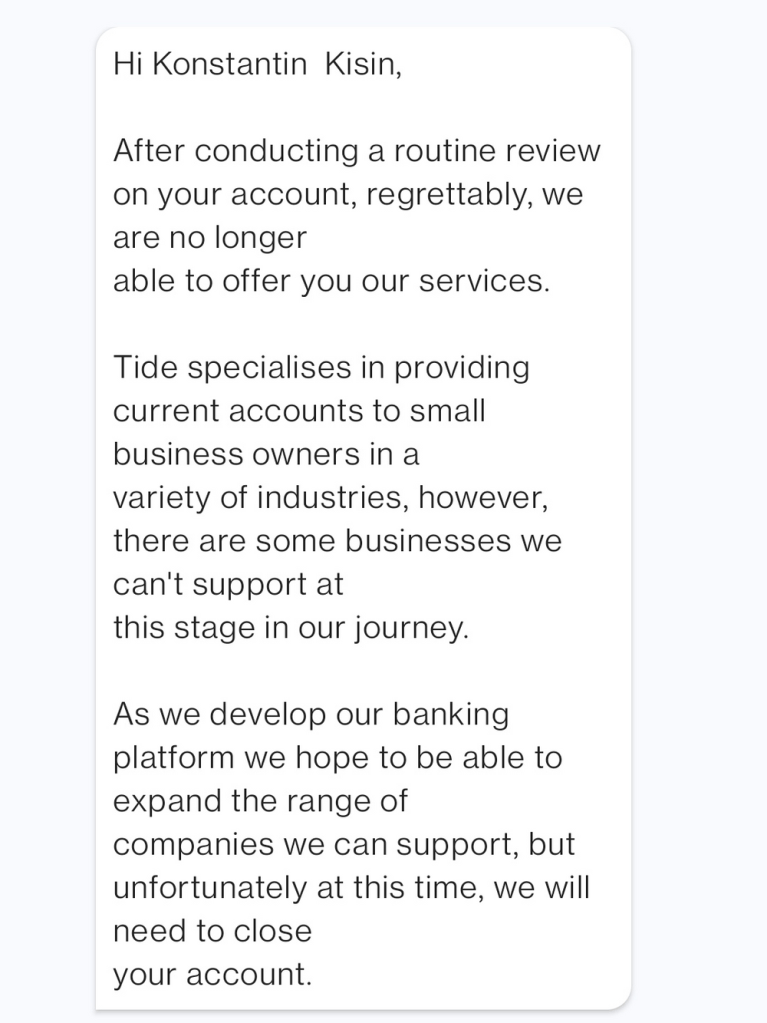

Recently Konstantin Kisin (a UK comedian/commentator) got a message from the company that was acting as his bank for a podcast he does with some other people.

There then followed a certain amount of hilarity as Mr Kisin asked (not unreasonably) for a reason why and received a number of non-answers.

There are some interesting curlicues to this case though.

Starting with the fact that the “bank” isn’t actually a bank. There’s nothing wrong with that, what they’ve done is partnered with a couple of actual banks to offer a banking service that is more convenient for small businesses than that offered by a traditional bank. This is no doubt one reason why Mr Kisin decided to use them. However it probably gives them rather more flexibility to discriminate that they would have if they were an actual bank.

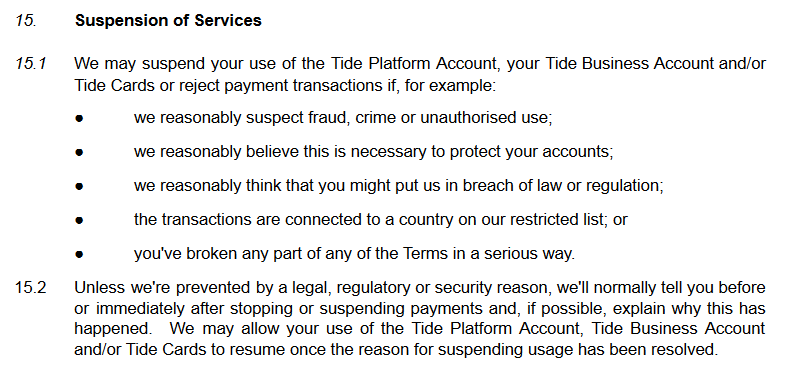

Mind you in the T&Cs there’s this:

So it would seem that the lack of initial explanation means there’s a “legal, regulatory or security reason” for the decision. Now, as someone who works in cyber-security, I can say that this vagueness is typically there so that the company has a get out when closing an account for a “Nigerian Prince” that offers exciting opportunities to for suckers to work from home while enriching some Eastern European cyber-criminals. BUT short of Mr Kisin running a scam, which seems unlikely given his relatively high public profile in the UK, and given that the account seems to be tied explicitly to a locals account where he and a colleague do video interviews for subscribers the “involved in (cyber)crime” excuse seems highly unlikely.

So the more likely reason is that the “bank” doesn’t like Mr Kisin’s generally unwoke and skeptical viewpoint on matters and is now desperately trying to retcon a reason. Quite possibly the root cause is that some SJW activists figured out that Kisin used Tide as a banker and caused some regulatorily complex work to be done on his account which meant that Tide was spending a lot more money responding to them than it could possibly make from Kisin’s account.

I should note that the excuse about third party payment processors and validation simply doesn’t pass the giggle test. TRIGGERnometry uses Stripe (as part of its locals based subscription service) and Paypal (linked from twitter and youtube for donations and in the shop part of the website) and as far as I can tell that’s it. Lets start with Paypal, which has had its own free speech issues (see this for example), and which seems more likely to be the source of donations. Paypal knows the email address and credit card (or bank account) details (including the address) of everyone using it and there is no effective difference (to the recipient’s bank) to a payment made for a purchase of goods/services and a donation. Moreover it stretches credibility that no other Tide customers are using Paypal to receive payments.

That’s the very slightly more plausible 3PPP. If Tide has problems with Stripe then I guarantee that TRIGGERnometry is far from the only organization that banks with Tide that uses Stripe. Stripe is ubiquitous and one of the reasons for this is that it is very good at reducing fraud, which it does by precisely the sort of validation that Tide says it can’t trust. Now I suppose there’s the vague possibility that somewhere on an older website that I can’t find the TRIGGERnometry people have a different payment processor, but that seems unlikely. Aside from anything else if one particular 3PPP was problematic, the obvious thing for Tide to do is to mention that they have a problem with 3PPP X.

Since, rather than say that, they originally gave notice of closing the account and only a week or so later came up with 3rd Party Payment excuse we can be almost certain that Tide simply don’t want TRIGGERnometry’s custom but aren’t willing to come out and say so.

Anyway, moving on. In one of the threads on twitter discussing this there was reference to an excellent, but older, thread by Patrick McKenzie (of Bits About Money):

This is a problem that has worsened as governments (and particularly the US government) have passed more and more regulations to prevent money laundering, sanctions busting (and increased massively the number of entities sanctioned) and so on. What this means is that banks have to employ office buildings full of expensive lawyers, compliance officers and the like and they can track what accounts they work on and how much money they earn from those account holders. Since most checking/savings accounts earn the bank a few dozen dollars a year, the handling cost of generating a single Suspicious Acitivity Report (SAR) can wipe out a decade or more of income. Effectively if your bank has to do anything manual and out of the ordinary because of a possible problem with your account they will put a strike on it and, unlike baseball, in banking it’s usually two strikes and you’re out.

Unless, it seems, your name is Biden

Hunter Biden, or a combination of Hunter, Joe and James and their various associated companies, has accumulated 150 SARs most (all?) since 2008 – so an average of about 10 a year. Now it is undoubtedly true that some of these are simply because the amounts being transferred are in the $millions range from foreign entities and are somewhat routine but others almost certainly are not. And the fact is that not all $million transactions from places like Romania or China generate SARs in the first place – or at least they used not to. But one might wonder why banks seemed willing to continue to allow the Biden family to do business with them when random gentlemen called Mohammed (name per McKenzie – one suspects that the problem is limited to people with such names) are invited to take their business elsewhere after just one or two such interactions.

Of course actually we don’t wonder at all. We know why. It’s because not doing business with a Biden would result in even more expensive legal work as Biden and his fellow democrat and deep state allies would cause banks to appear before congressional committees, respond to regulatory questions from the SEC and so on. This is not the case if you are some random Tom, Konstantin or Mohammed who lacks the connections to the government and bureaucracy.

In these days of ubiquitous electronic payments, not having a bank account and/or credit/debit card is a big problem. In Kisin’s case it seems other banks have stepped forward who are quite willing to accept his business but that may not always be the case. As people like the FSU found out with Paypal, or the Canadian truckers found out with various platforms, if any part of the payment process decides they don’t like you then you can be out a lot of money. Worse the byzantine T&Cs that you have to accept to get any kind of money may allow the company to keep the money in limbo for a few months and even levy a fine for doing/saying something they disagree with.

In many cases getting a satisfactory resolution or even any kind of answer requires the glare of publicity rather than calling someone to find out what the problem is. Indeed many internet companies make it extremey difficult to talk to an actual human. let alone one who can give you a straight answer. Effectively, unless you happen to have a senior politician like an MP or US senator who can ask questions for you, your money can be arbitrarily withheld and you will be unable to get anyone to tell you why or give you your money back in a timely manner. On the other hand if you do have friends in high political places you can get a pass on transfers that do in fact raise precisely the sorts of questions that the vague “validation” phrases refer to.

The financial system has become, in effect, weaponized against people who rock the boat and in favor of people who are well connected. This is a problem. Possibly Musk’s X corp will include payment processing that is not limited to particular points of view and the like, but it’s dangerous to rely on a single billionaire to keep the world free, even if he is probably the richest man in the world.